Book review: The Power Law

Review

My notes below this review might seem long, but The Power Law contains a wealth of information that didn’t make it to this post. I also absorbed a large amount of tacit knowledge that’s hard to put into words. For example, I formed a general opinion of a number of players in the venture capital (VC) industry, a sense for what kind of help VC firms provide beyond capital, etc. I can recommend reading the book if the subject interests you.

To balance the frank approval of the successes of venture capital, there are fairly many failure stories in the book. WeWork, Theranos and Uber are splashy examples, but there’s also the more “boring” failure story of pen-computer company GO, which was a bet on clearing a certain technological barrier that just didn’t pay off; Kleiner Perkins’ ill-advised cleantech bets and diversity hiring efforts; Andreessen Horowitz’s lackluster performance due to their insistence on hiring ex-entrepreneur partners; and Masayoshi Son’s Hail Mary investing style.

Mallaby writes well. His prose boasts stylistic flourishes on the sentence level (“Noyce came from … the Midwest, where the land was as flat as the social structure”), and clarity on the paragraph level. He backs an impressive number of (often juicy) claims with “[some dotcom giant founder]’s email/interview with the author” in the references. For example, the Yahoo founder Jerry Yang apparently joked with Mallaby that he had considered changing his company’s name, since “Sequoia’s star investments had five-letter names: Atari, Apple, Cisco”.

I recently watched a video essay about how documentaries like Pumping Iron lie to serve a narrative; often, the documentary’s overarching narrative is decided before the first scene is shot. I also learned only lately that the story about Jeff Bezos leaving DE Shaw after reading Remains of the Day is false, and the one about Pierre Omidyar founding eBay to help his girlfriend find the Pez dispensers she collected is a PR invention (at least according to this article). These have made me more skeptical of SV legends. The Power Law mentions more than one example of a VC helping his founders become public figures: Mike Moritz with Yahoo’s Jerry Yang and WhatsApp’s Jan Koum, for instance. Remains of the Day- and collector girlfriend-type legends establish a mythos around the founder that can only help the VCs in this mission. So, it’s important to take Silicon Valley legends with a grain of salt—especially in this book, which relies for some of its facts on first-hand accounts.

Why is California the world’s tech hub?

Mallaby argues there are three popular (but incorrect) explanations for why California became Silicon Valley:

- Stanford: While having a premier research university that could generate basic science research was certainly useful, Boston had two excellent universities—MIT and Harvard—while Pittsburgh had Carnegie Mellon. Neither city became an innovation hub. (Though Paul Graham does consider CMU a major reason why Pittsburgh has potential for becoming a startup hub.)

- Federal defense funding: While SV firms received some defense money, the military-industrial complex was located primarily on the East Coast. Millions of dollars flowed to Pentagon-backed research centers around Boston, and by the late 1960s over a hundred tech startups had spun out of these labs. Vannevar Bush, who controlled this complex as head of the US Office of Scientific Research and Development, was the dean of MIT’s School of Engineering.

- West Coast anticorporate counterculture: The story goes that the West Coast’s hippy vibe inspired founders “to share ideas rather than run to the nearest patent lawyer” and be “open to any unkempt upstart who might see something, sense something—something with the potential to change everything”. But the “hacker” ethic actually originated in MIT’s Tech Model Railroad Club. Linus Torvalds created Linux, the world’s most famous open-source project, in Finland. (Actually, Linux is maybe second most famous—after Python, which Guido van Rossum built in the Netherlands). However, neither Cambridge nor northwestern Europe became the sort of innovation hub that SV did.

Mallaby says that the Valley really became a tech hub because there “the patina of the counterculture combines with a frank lust for riches”.

Two rich East Coast families—the Whitneys and the Rockefellers—had dabbled in funding risky ventures, but their motivations were patriotic and philanthropic rather than profit-seeking. Boston labored for years under American Research and Development, Georges Doriot’s venture fund, which was unfortunately structured as a public company that couldn’t grant employees stock options. Doriot underpaid his employees and wrested equity away from his founders (like Ken Olsen and Harlan Anderson of the immensely successful Digital Equipment Corporation). “Capital gains are a reward, not a goal,” he had declared.

In contrast, Arthur Rock and Thomas Davis’ partnership ensured that the partners, founders as well as employees (for whom usually 10% of the stock was reserved) would be compensated in equity, since Rock had witnessed first-hand the positive effect of compensation in equity on Fairchild Semiconductor’s culture. Davis & Rock was driven from the start to make profitable, rather than philanthropic, investments. To this end, they made several financial innovations described in the next section. Following in their footsteps, their successors in Silicon Valley placed profit above patriotism.

I am reminded here of Paul Graham’s essay on cities: “In a hundred subtle ways, the city sends you a message: you could do more; you should try harder. … What I like about Boston (or rather Cambridge) is that the message there is: you should be smarter. You really should get around to reading all those books you’ve been meaning to. When you ask what message a city sends, you sometimes get surprising answers. As much as they respect brains in Silicon Valley, the message the Valley sends is: you should be more powerful.”

Venture capital in the 1960s

Liberation capital

Arthur Rock

on the TIME

cover in

1984.

Arthur Rock

on the TIME

cover in

1984.

Davis & Rock decided not to diversify, but rather make concentrated bets in a handful of companies. This flew in the face of portfolio theory, but they thought it would be acceptable for two reasons. First, to justify the unusually high risk in backing startups—most new companies crash and burn, after all—they decided to only fund those that could plausibly yield >10x returns. Second, as owners of just under half of a firm’s equity, they would get a board seat and the right to steer the firm’s strategy when it veered off-course. The overall effect would be that of reducing the financial risk.

To avoid repeating Doriot’s mistake with ARD, the fund wouldn’t continue indefinitely, but would rather be liquidated after 7 years. This would incentivize the partnership to act with urgency and aggression; but as a counterbalance to this aggression, Davis & Rock would invest their own money in the fund as general partners. Meanwhile, their limited partners would invest but not participate in the fund’s day-to-day operations.

Further, the partnership would only ask for equity in exchange for money—not offer startups loans, or anything else.

When Davis & Rock wound up their partnership in 1968 after the pre-decided 7 years, their return was 22.6x, eclipsing Warren Buffett’s in this period, as well as that of the inventor of the “hedged fund”, Alfred Winslow Jones. Just as Jones’ model birthed new hedge funds, Davis & Rock’s success inspired many other VC firms modeled after them—“equity-only, time-limited”. In 1969, \$171 million flowed into the sector, equivalent to fifty new Davis & Rock partnerships. Mallaby describes this as the birth of “liberation capital”, whereby disgruntled innovators (like the Traitorous Eight who left William Shockley’s company to found Fairchild) got access to an abundance of capital.

Afterwards, Rock helped Robert Noyce and Gordon Moore leave Fairchild to start Intel, while Davis founded Mayfield.

Venture capital in the 1970s and ’80s

In 1972, Davis & Rock enjoyed a threefold vindication: ARD closed, and two VC firms modeled after it started which would go on to become extremely influential—Sequoia and Kleiner Perkins.

Activist investing at Sequoia

Sequoia was founded by Don Valentine, who had grown interested in VC after rising through the ranks at Fairchild. He decided against raising money from Wall Street because he hated “people with hyphenated names or roman numerals after their last name, direct descendants of immigrants who arrived on the Mayflower, people who had enjoyed living on the East Coast, and those who wore Hermès ties, suspenders, cuff-links, signet rings, and monogrammed shirts”. (The one time he tried Wall Street—the Salomon Brothers—he got asked “What business school did you go to?” Valentine replied, “I went to Fairchild Semiconductor Business School.”)

Eventually, Valentine raised money from foundations and university endowments which enjoyed charitable status, like Ford Foundation, Yale and Harvard. Mallaby argues this created “one of the great virtuous cycles of the American system”: VCs backed knowledge-intensive startups, and some of the profits flowed to research institutions that generated more knowledge. In 1990, Yale made the first university investment in a hedge fund, Farallon Capital, “extending the role of college endowments in nurturing cutting-edge investment methods” according to Mallaby. To this day, the conference rooms at Valentine’s old firm are named after their main limited partners: Harvard, MIT, Stanford, etc.

(Side note: I really need to read more about college endowment management; it sounds very interesting. AFAIK, professors of finance often manage the fund. It would be interesting to see how quickly new techniques/practices in portfolio management theory are introduced after their invention into the managers’ style, and if endowment management differs from more traditional wealth management as a result of the managers’ academic background.)

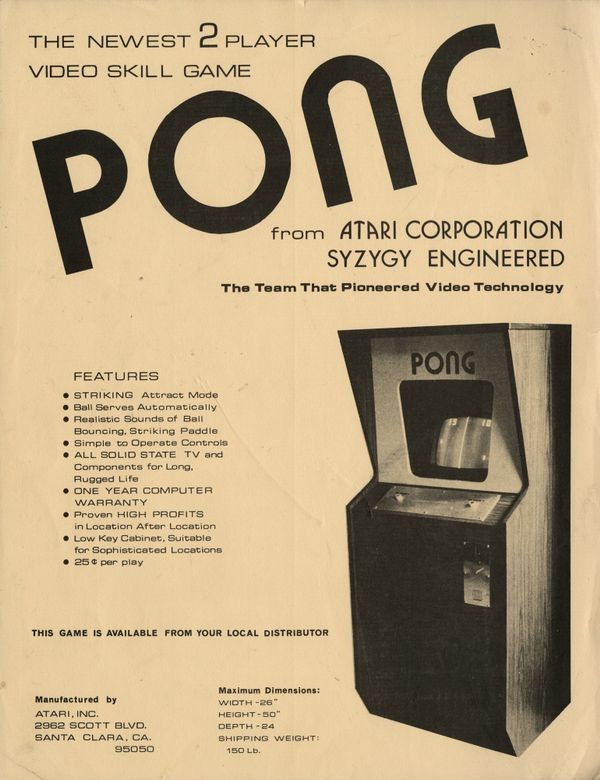

Sequoia’s breakthrough investment was Atari. Founded by Nolan Bushnell in 1972, it rode on the back of the hit game Pong and generated impressive revenues, but was poorly-run: “employees got travel expenses paid in advance and sometimes absconded with the cash, never to be seen again”, while “[c]ustomer orders were frequently not written down, making costly disputes commonplace”.

Valentine proposed a gradualist approach to investing in Atari—he would invest on the condition that Atari develop a family version of Pong (moving from bars, the small market they previously competed in, to families, a vast market), and secure a powerful distributor. He could dictate his terms because of the 1970s stagflation, which had reduced the number of competing VCs. This marked the beginning of activist investing, where investors take an active approach to steering company policy (Rock had been hands-off in comparison with Fairchild, Scientific Data Systems, Teledyne and Intel).

A 1972 advertisement for

Pong directed at owners of bars and pinball arcades, via the Computer History

Museum.

A 1972 advertisement for

Pong directed at owners of bars and pinball arcades, via the Computer History

Museum.

After Atari developed Home Pong and partnered with the retailer Sears, Valentine’s terms had been satisfied and he invested in the company. But when Atari engineers envisioned the next breakthrough—a console that could play not just Pong, but multiple games—they estimated they needed an investment of up to \$50 million. Since the stock market had dried up, Atari couldn’t go public.

So, Valentine proposed that Atari should be sold to Warner Communications. Nolan Bushnell presented stiff opposition. Mallaby’s story of how Bushnell was convinced is marvelous:

Steve Ross, the founder and chairman of Warner, invited Bushnell to New York to discuss a deal. Valentine made sure he was invited also. In late 1976, a Warner company jet fetched Bushnell and Valentine from California. On board, they were greeted by Clint Eastwood and his girlfriend, Sondra Locke; Eastwood graciously made Bushnell a sandwich. When the plane touched down in Teterboro Airport, a limo ferried the Atari people to suites in the Waldorf Towers hotel. That evening there was a dinner at Steve Ross’s palatial apartment, and the group watched an unreleased Eastwood movie together. By the end of the day, a starstruck Bushnell had agreed to sell Atari for \$28 million.

(The sandwich is impressive, but it’s the unreleased Eastwood movie that makes it art.)

And the sandwich was a deliberate flourish. According to a footnote: “Valentine recalls, ‘That was the highlight of Nolan’s trip. It was not an accident that he made Nolan a sandwich. He didn’t make my sandwich. He made Nolan a sandwich.’”

Startup incubation at Kleiner Perkins

Meanwhile, Eugene Kleiner (of the Traitorous Eight, who left Shockley to start Fairchild) partnered with Tom Perkins, a former general manager of HP’s computer divisions, to create Kleiner Perkins, a new VC firm.

Kleiner Perkins’ early investments were unspectacular due to the ’70s stagflation, inspiring them to adopt an even more hands-on version of Valentinian activist investing: they would hire junior associates and kick ideas around with them, and KP would fund the startups born from these discussions. KP became probably SV’s first startup incubator.

One of Kleiner Perkins’ first hired “entrepreneurs in residence” was Jimmy Treybig, whose idea was to borrow from aircraft design and build “a computer system with backup processors so that one engine could fail without the whole thing crashing”.

Treybig’s idea would almost certainly be profitable, since “[c]omputer crashes that destroyed data and brought business to a halt were horribly expensive”. So, the market risk was low, but the technical risk of successfully building an operating system that could switch processors in a crash was great: an inversion of Atari, which had low technical risk (they used primitive tech) and high market risk (they weren’t sure if people would like their games). In general, KP tended to fund projects with high technical rather than market risk after funding Treybig’s firm Tandem. Perkins stated a “law”: “market risk is inversely proportional to technical risk,” because if you “solve a truly difficult technical problem, you will face minimal competition”. (I don’t think this “law” is true, because you still need good market sense to choose the right technical problems; SixthSense and many late 20th-century questions in theoretical physics were hard technical problems, but didn’t lead anywhere useful AFAICT.)

(By the way, Treybig says VCs want to find out one thing: “Why is this a big market, and how are you going to build a really strong position in it?” I think this is a really succinct way to express VC investors’ interests.)

A seed investment by Kleiner Perkins paid for technical consultations that ironed out Treybig’s technical challenges, and established Tandem Computers. Despite this, Arthur Rock, Venrock (the Rockefeller family’s investing arm), et al, passed on the opportunity to invest in Tandem. It was illogical: with the technical risk gone, the product was sure to be profitable. However, the conventional wisdom stated that taking on the computer company IBM was suicide (this is why Arthur Rock had been hesitant to fund Scientific Data Systems).

So, Kleiner Perkins itself invested \$1mn in Series A funding in Tandem. If the bet hadn’t paid off, there likely wouldn’t be a second KP fund. Fortunately, Tandem made a \$150mn windfall, dwarfing KP’s combined \$10mn return on its first nine investments (a demonstration of the power law in VC returns, after which the book is titled).

After Treybig vacated the junior associate position at KP, he was replaced by Robert Swanson. Swanson saw potential for manufacturing life-changing drugs with recombinant DNA, a new technology. He convinced Herbert Boyer, the technology’s inventor, to found Genentech with him. The company acquired funding and hired scientists at breakneck pace, freeing Boyer from writing grant proposals for modest sums.

Genentech’s founders Herbert

Boyer and Robert Swanson, via

Genentech.

Genentech’s founders Herbert

Boyer and Robert Swanson, via

Genentech.

Perkins de-risked Genentech’s speculative technology by suggesting that it not hire scientists or build a lab early on, but contract the work out to existing labs (another example of activist investing). Before engineering a bacterium that could synthesize insulin, Genentech’s scientists decided to engineer a bacterium that could synthesize somatostatin, a smaller hormone. Both of these were in line with Perkins’ desire to remove the “white-hot risks”, or the uncertainties that most threatened to derail the project, first.

A step-by-step approach remains good advice for hard tech startups, as Sam Altman explains in this lecture at MIT.

Scientists Swanson had consulted with before starting Genentech had estimated rDNA would take decades to commercialize. A mere two years after Genentech was founded, “a press conference announced the production of artificial insulin to an astonished nation”.

Before Genentech synthesized human insulin, the only way to produce the drug was to press it out of cow and pig pancreases. Some people were allergic to pig insulin—the synthesis of human insulin gave them a new lease of life. The story of Genentech is one of the clearest cases of venture capital doing good.

Both Sequoia and KP went beyond just providing capital; Valentine’s counsel was almost indispensable to Atari, while KP’s focus on eliminating white-hot risks by bringing in technical consultants for Tandem and outsourcing experiments for Genentech proved useful.

Mallaby sums up their contribution as “[e]arly risk elimination plus stage-by-stage financing”.

Sequoia’s Cisco home run

An even more stark example of activist investing is Don Valentine’s investment in Cisco. Its founders and the management were so combative that at one point, Valentine had to bring in a company psychologist whose role “was not necessarily to cause us to love one another, but to avoid us taking physical action against one another” like engaging in literal fistfights. Had Valentine not brought new management on board, and eventually ejected the founders after Cisco engineers soured against them, Cisco might have disintegrated. Cisco eventually generated Sequoia’s first >\$100mn gain from a single investment.

![]() Cisco is named after San

Francisco, and its logo is inspired by the Golden Gate Bridge. Cisco’s

reasoning

for the logo choice: “Back in the late 1800s, the only way to cross the bay was

by ferry. … On May 27, 1937, the Golden Gate Bridge finally opened, connecting

San Francisco and Marin for the first time. Back then, we built bridges to

connect different parts of the bay. Since then, we have built technologies to

connect classrooms in schools K-12 and universities around the world.”

Cisco is named after San

Francisco, and its logo is inspired by the Golden Gate Bridge. Cisco’s

reasoning

for the logo choice: “Back in the late 1800s, the only way to cross the bay was

by ferry. … On May 27, 1937, the Golden Gate Bridge finally opened, connecting

San Francisco and Marin for the first time. Back then, we built bridges to

connect different parts of the bay. Since then, we have built technologies to

connect classrooms in schools K-12 and universities around the world.”

On the other hand, Cisco’s competitor Wellfleet lost its lead. Their founder was too reluctant to bring products to market that he considered unperfected. East Coast VCs deferred to the respected inventor’s judgment, presenting a stark contrast to SV activist investing.

It was VCs’ networks that helped them land deals, and connect executives and developers to their ventures. On the importance of networks, Mallaby argues that companies in Japan and Boston were self-contained and vertically-integrated, which led them to waste ideas by bottling them up. In contrast, SV had a culture of “coopetition”: small competing firms without a taboo on their employees helping each other on, for example, technical problems.

This argument comes from AnnaLee Saxenian, who in turn is drawing from a highly-cited paper by Mark Granovetter arguing that a plethora of weak ties generates a greater circulation of information than a handful of strong ones. The weak ties between flat SV startups afforded the region success that the vertically majestic buildings of Boston and Japan couldn’t replicate.

Venture capital in the early 1990s

The logic of backing Internet companies

Kleiner Perkins partner John Doerr in 1984,

via Fortune.

Kleiner Perkins partner John Doerr in 1984,

via Fortune.

John Doerr, a partner at Kleiner Perkins, knew that sometimes, technologies grow exponentially (ie, become exponentially faster, cheaper or higher-yielding) because they are founded upon technologies that themselves grow exponentially. For example, as an engineer at Intel, he noticed “how Moore’s law transformed the value of companies that used semiconductors: the power of chips was doubling every two years, so startups that put them to good use could make better, cheaper products”. The chips inside a modem, digital watch, or PC would get 50% cheaper in two years, 75% in four, and so on; thus, the firm’s profits could grow exponentially.

Now, Doerr heard of Metcalfe’s law: that “the financial value or impact of a telecommunications network is proportional to the square of the number of connected users of the system” (from Wikipedia). (This is because the number of connections between terminals connected to the system rises quadratically as new terminals are added; given Dunbar’s number, this effect eventually plateaus, but it is still quite powerful.)

Metcalfe’s law was even more explosive than Moore’s law, because “[r]ather than merely doubling in power every two years, as semiconductors did, the value of a network would rise as the square of the number of users. Progress would thus be quadratic rather than merely exponential; something that keeps on squaring will soon grow a lot faster than something that keeps on doubling. Moreover, progress would not be tethered to the passage of time; it would be a function of the number of users.”

What’s more, Metcalfe’s law would stack with Moore’s law, which would’ve been powerful enough alone.

So, any technology that made itself indispensable to Internet users would enjoy the tailwinds of both Metcalfe and Moore’s laws. The browser Netscape was exactly that technology, since it made accessing the Internet so much simpler. KP made an eye-watering 100x on Netscape.

Venture capital in the late 1990s

Reaping “beta” and skimming “alpha”

In 1996, Masayoshi Son of Japan’s SoftBank invested \$100mn in Yahoo, heralding the rise of “growth investing”. Yahoo was then engaged in a capital-intensive advertising war with its rivals which made Son’s offer extremely attractive. But Son had also brandished a stick to go with his carrot: he told Yahoo that if they didn’t accept his \$100mn investment offer, he would make the same offer to their rival. Whoever had the larger advertising budget would dominate the market. No SV VC would’ve made a Corleonesque threat like that, since they had a reputation to preserve and long games to play; but Son was an outsider.

Son reaped a stunning \$150mn in the Yahoo IPO weeks later. He was the first VC since Valentine to make >\$100mn on a single venture (Cisco), and had done it without the heartache of tearing down and rebuilding a management team. By pouring similarly astronomical amounts into startups, he made \$15bn between 1996 and 2000, becoming the first VC on the Forbes billionaire list. He continued to spray capital on several startups; his success with Yahoo, Mallaby argues, was closer to a lucky hit than a carefully-considered bet.

In contrast, Benchmark was a small fund, but it made \$5.1bn on a mere \$6.7mn investment in 1997 in eBay. In summer 1999, Benchmark’s portfolio was worth \$6bn, implying an impressive 25x return. Mallaby cites this as an example of the “back-to-basics” investing style working, “whatever the message from Masayoshi Son’s example”.

Borrowing from hedge fund terminology, Mallaby says that Son was reaping “beta”, the financial benefits of merely staying in the market, while Benchmark earned “alpha”, the financial rewards of “beating” the market.

Bruce Dunlevie of Benchmark has a memorable quote:

What’s venture capital? It’s sitting at your desk on Friday at 6:15 p.m., packing up to go home when the phone rings, and the CEO says, ‘Do you have a minute? My VP of HR is dating the secretary. The VP of engineering wants to quit and move back to North Carolina because his spouse doesn’t like living here. I’ve got to fire the sales guy who’s been misreporting revenues. I’ve just been to the doctor and I’m having health problems. And I think I need to do a product recall.’ And you, as the venture capitalist, you say, ‘Do you want me to come down now or get together for breakfast in the morning?’

The rise of the angel investor

Andy Bechtolsheim (second from

right) with his fellow Sun Microsystems co-founders including Vinod Khosla

(left) in 1982, via The New York

Times

Andy Bechtolsheim (second from

right) with his fellow Sun Microsystems co-founders including Vinod Khosla

(left) in 1982, via The New York

Times

According to Mallaby, the Sun Microsystems co-founder Andy Bechtolsheim wrote the Google founders a generous \$100,000 check without asking what share of the company he was buying, and set the precedent of the angel investor in the Valley that was as historic as Son’s \$100mn investment.

In 1998, Brin and Page raised >\$1mn from four angels, more than Yahoo had raised from Sequoia less than five years earlier. Further, Google’s angel investors like Bezos and Bechtolsheim were too focused on their own companies to worry about how Google was getting on.

Now, company founders had an alternative to traditional VCs if they felt that would be giving away too much control—much as Son’s growth-capital checks offered a partial alternative to going public and losing some control over the startup. Entrepreneurs like the Googlers could now raise “money like that, kind of for nothing [by way of investor control]”. Mallaby claims that “[n]ever in the history of human endeavor had young inventors been so privileged”.

Later, Khosla of KP invested in Google because he believed that “engineering products could improve more than non-engineers imagined”, having invested profitably in three successive generations of routers because he saw room for improvement in their engineering when most others didn’t. He thought a latecomer to the search market like Google could blow out the competition if it had significantly better algorithms.

Google managed to raise capital from both KP and Sequoia, in a testament to the growing negotiating power of founders in the Valley.

Venture capital in the 2000s

Tiger’s hedge fund/VC hybrid model

Tiger Global’s hedge fund background drove them to make interesting decisions. For example, most VCs chase startups that are being chased by other VCs. There’s a logic to this pack mentality: VC buzz can attract talented managers/developers and important customers, both of which make a company more attractive to VCs, strengthening a positive feedback loop. But when outsider Tiger heard that some Chinese companies which seemed like good deals had gone unnoticed by SV VCs, rather than hesitating, they doubled down: their former boss had taught them that “shares were most likely to be mispriced when nobody was scrutinizing them” and “if you liked a stock but other professional investors did not own it, this was a good sign; when the others woke up, their enthusiasm would drive your stock higher”. These investments generated 5x-10x returns.

Tiger’s founders came around to private tech investing with an interesting perspective on why long betting is superior: “A great short position could make you a maximum of 100 percent, if the company went to zero. A great long position could make you five or ten times capital.” Or, as founder Chase Coleman put it: “Why do twice as much work to make half the profit?” Tiger forwent the luxury of betting short.

They also avoided localizing themselves to a geographic region like SV VCs were wont to do, taking a cue from Julian Robertson of their parent hedge fund Tiger Management, who had said that the “best investments were often to be found abroad, where Wall Streeters were thin on the ground and local investors were unsophisticated”. More pithily: “Why would I sit here and try to hit major-league pitching, if I can go to Japan or Korea and hit minor-league pitching?”

They made a conscious decision after investing in three home-run Chinese copycat companies to invest in “companies that implemented a proven business model in a particular market”: the eBay of South Korea or the Expedia of China, or more generally, “the this of the that”.

Mallaby illustrates a benefit of the hedge-fund mindset: when Ctrip increased its valuation after SARS despite an agreement with Tiger to sell at a SARS-discounted price, another VC might’ve called off the deal at the breach of trust. But Tiger recognized that “[a] higher valuation matched by higher revenues left the price-earnings ratio unchanged”, so it went ahead and reaped a gigantic \$40mn profit in 2003.

However, Mallaby attributes Tiger’s decision to pass on Alibaba to this same difference between venture thinking and hedge-fund thinking. As Ma was then planning to pivot to a completely different market, Alibaba didn’t fit the “the this of the that” mold. A VC might’ve invested in the company anyway, looking at Ma’s character and his team’s quality, but Tiger’s “focus on metrics such as incremental margins” blinded it to the value of “entrepreneurial genius”, Mallaby argues.

YC and Founders Fund

The first Y Combinator batch, via

YC.

The first Y Combinator batch, via

YC.

Remarkably, before Paul Graham’s 2005 “Summer Founders Program”, no angel had thought to structure investing in batches. But batch processing was “marvelously efficient”: “The batch members would provide support for one another, relieving the burden on himself and Livingston. And YC could help the startups as a group. It could invite a speaker to a dinner and have all its protégés listen. It could organize a single demo day at which all its founders would pitch to follow-on investors.”

Bristling at what he perceived as mistreatment by Mike Moritz at PayPal, Thiel soured on traditional VC and set up Founders Fund in 2005. Sean Parker, who had been ousted from Facebook by Accel and stripped of a large fraction of stock for a debacle involving drug abuse with his underage assistant (which is dramatized in the last few scenes of The Social Network), joined Thiel. Thiel’s thesis was that VC coaching was useless at best, and damaging at worst (since it involved bringing tried-and-tested methods to would-be outliers).

The fall of KP and the rise of Accel

Meanwhile, KP’s Doerr made a bet on cleantech, starting in 2004. His intellectual counterweight Khosla had left, with no one to fill the vacuum. Khosla was against cleantech investments, not least because they were extremely prone to political developments.

To compensate for the large capital requirements and long time frames of hard tech startups, Doerr could have invested at lower valuations and demanded additional equity for his money. But because of the rising “founder-friendliness” entrenched by youth revolts like Facebook’s, Doerr didn’t.

After the government failed to deliver on promises of instituting carbon taxes, KP’s performance dulled: whereas in 2001 Khosla and Doerr had ranked first and third respectively on the Forbes Midas List, by 2021 Doerr came seventy-seventh, while no other KP figure made it to the top hundred.

Despite Doerr’s enthusiasm for diversity, many women he recruited found his firm’s culture unwelcoming and biased against them. This culminated in Pao v KP, which KP won, but with its reputation tarnished. Doerr also felt comfortable recruiting seasoned executives/politicians like Colin Powell and Al Gore. In contrast, Accel hired fewer women but empowered them to higher positions, and hired younger investors who could hustle with emerging startups. (Perhaps they’d agree with Sequoia’s Mike Moritz, who said of fifty-something seasoned executives: they “had been too successful, had lost some spring in their step, were not hungry enough, had too many outside commitments and, most of all, were not prepared to become rookies again”.)

Accel had many successful partners, not just one or two superstars: “Its top seven investments, each generating a profit of more than \$500 million, were led by seven different partners—or actually eight, because one was a two-person effort.”

Accel’s senior investors had a practice of occupying a startup board seat with a junior partner as an understudy. After the understudy grew more confident, the senior partner would leave the board seat for them. This way, if the startup foundered, the senior partner would take the fall. This was in marked contrast to KP’s approach, where senior partners reportedly swooped in to take board seats (and thus, credit) from younger investors who had closed the deal.

Andreessen Horowitz

Marc Andreessen, via The

New

Yorker.

Marc Andreessen, via The

New

Yorker.

After a streak of angel investments, a venture fund seemed the logical next step to Marc Andreessen (of Netscape glory). But he recognized that his fund had to differentiate itself: “Accel had differentiated itself by specializing in certain fields; Benchmark had pitched its ‘better architecture’ of high fees and small funds; Founders Fund had pledged to back the most original and contrarian companies.”

For their part, Andreessen and Horowitz promised to extensively coach technical experts in the nuances of being chief executives: “how to motivate executives, how to rally sales teams, how to sideline a loyal friend who has poured all his energy into your company”. Also, every partner at their firm would have entrepreneurial experience.

Mallaby argues:

Of course, Andreessen’s pitch was less original than he pretended. Many venture capitalists—nearly all the early Kleiner Perkins partners, not to mention Thiel, Graham, Milner, and others—had entrepreneurial experience. The idea of coaching founders was not original, either. Nor was it even clear that entrepreneurship was the best background for a venture capitalist. An entrepreneur typically had worked at just one or two outfits, whereas VCs who had joined the investment business young had been in a position to see under the hood of dozens of startups.

(Andreessen himself mused in 2007: “There’s probably still no substitute for the VC who has been a VC for twenty years and has seen more strange startup situations up close and personal than you can imagine.”)

According to Mallaby, Andreessen Horowitz’s distinguishing strength was that despite being “a product of the youth revolt, a16z was not necessarily founder-friendly. It aimed to help technical founders succeed, but if they were set on doing the wrong thing, it had no problem confronting them. Peter Thiel’s fund had never opposed a founder in a board vote, and Milner did not even take board seats. But Horowitz was more hands-on: he combined the faith in scientific founders of Paul Graham with the toughness of Don Valentine.”

For example, Horowitz persuaded the Nicira CEO not to grab the first acquisition deal that came his way. By waiting it out, the company’s valuation doubled. Similarly, he effectively vetoed the Okta CEO’s decision to hire a marketing officer he liked who would’ve been risky.

a16z initially did well, but barely outperformed the S&P 500 in late 2018; Mallaby claims most of this underperformance can be explained by their insistence on hiring ex-entrepreneurs. In 2018, when a16z hired its first non-ex-entrepreneur general partner, Horowitz said: “It’s a kind of a big thing for especially me to eat crow on. It took probably longer than it should’ve to change it, but we changed it.”

Mallaby explains: “The VC firms that launch with a splash tend to have two things in common. They have a story about their special approach, and they have recognizable partners with strong networks.” Sometimes, the novel approach really is what causes their success: Milner’s spreadsheets, Tiger’s hedge fund roots, YC’s batch-based seed investing. But more often, “new venture firms succeed because of the founders’ experience and status.”

Mallaby says a16z’s story illustrates this: Andreessen and Horowitz’s towering SV celebrity landed them lucrative deals, but later, as they diluted their own talent by hiring additional partners, “it found that some did not work out: being a founder is not the same as being able to pick which founders to invest in”.

Venture capital in China

From Alibaba’s Jack Ma begging Goldman Sachs for capital to Meituan’s Wang Xing being aggressively courted by a firm no less than Sequoia, China’s tech scene has evolved like California’s: there is now a surplus of capital and a relative dearth of good founders.

In China, since law forbade US ownership of internet companies and employee stock options, US VCs incorporated them in the Cayman Islands: “Goldman Sachs was forbidden to invest in an internet startup in Hangzhou, but it could buy shares in its Cayman parent”, and Cayman allowed for every kind of stock ownership.

Sequoia’s leaders Moritz and Doug Leone mentored Sequoia China led by Neil Shen and Zhang Fan hands-on, learning from Benchmark’s mistake in opening a London shop and giving them too much freedom—their European outpost had later declared formal independence and stopped sharing profits with California. Similarly, KP’s China shop had collapsed after Doerr, instead of mentoring it himself, delegated the job to his lieutenants. (It is an interesting question, BTW, which management technique has worked for VC shops more generally, ie, not just in China, but in Israel, India, and Europe too.)

Neil Shen, via The

Economist.

Neil Shen, via The

Economist.

The entrepreneur Wang Xing had tried aping known US successes, first Friendster, then Facebook and Twitter. Finally he struck gold copying Groupon, and erected the food delivery empire Meituan.

A Sequoia partner courted Wang incessantly: he “tried to get to Wang by speaking to his wife, who ran Meituan’s finances” and “befriended Wang’s co-founders and asked them to put in a good word for him”. Most strikingly, though, whenever he got the chance to speak with the hallowed founder, he “tried to talk about things that he’s not very familiar with, so we could add value”. (Mallaby adds: “Annoyingly, Wang had educated himself on an encyclopedia of subjects. It was hard to find a worthwhile topic that he hadn’t mastered already. … On a hike in September 2019, Wang asked the author [Mallaby] questions about his past books, but evidently knew most of the answers already.”)

(Of course, the logical next question is: what place on earth looks like China in the 1990s—full of capital-hungry entrepreneurs like Jack Ma, but with a dearth of VCs? India, many countries in Africa, and, to be sure, Ireland seem solid answers.)

China’s tech scene was copycat-happy to a comical extreme:

Having paid top dollar for its stake [in Meituan], Sequoia found itself caught up in an extreme version of the fight between X and PayPal. In 2011, an extraordinary five thousand group-buying websites sprouted in China … What became known as “the war of a thousand Groupons” ensued, with combatants splurging money on ever deeper discounts in order to attract users.

Eventually, Dianping emerged as Meituan’s only solid challenger.

The Meituan-Dianping meal-subsidizing and marketing war illustrates why mergers can be good for business: they eliminate zero-sum spending on advertising. At first blush, mergers seem bad from a public welfare perspective (customers get subsidized meals out of the competition!) but there are no free lunches; money VCs waste on advert wars could be usefully spent on biotech, space exploration, and other positive-sum startups.

Sequoia China has been extremely successful, investing in the ecommerce groups Alibaba, JD.com and Pinduoduo, and TikTok parent ByteDance. On 6 June 2023, however, Sequoia split its branches in the US, India (where their offshoot will now become Peak XV) and China (which will become HongShan, the Mandarin word for “redwood”). By March 2024, these entities will no longer share investors or returns.

Venture capital in the 2010s

Theranos

Interestingly, almost none of the money that Theranos raised came from Sand Hill Road VCs. Holmes’ meeting with the Californian VC firm MedVenture, which specialized in medical devices, ended with her leaving abruptly, unable to answer the investors’ questions. Tim Draper made an angel bet because of a family connection, but it was modest. But Rupert Murdoch, Walmart’s Waltons, Carlos Slim, et al, invested \$100mns.

WeWork

WeWork founder

Adam Neumann on the Forbes

cover

in 2017.

WeWork founder

Adam Neumann on the Forbes

cover

in 2017.

By buying stake in the buildings with which WeWork negotiated leases, the founder Adam Neumann was “[setting] himself up to profit personally from his company’s lease payments”: he was “effectively decoupling his personal fortune from his company’s profits, linking it instead to his company’s lease costs”, and as a result, “[a] gap between Neumann’s interests and his shareholders’ interests was opening”.

The business model at the heart of WeWork was sound—take out cheap long-term leases and rent out the space for short periods, at a markup—but to justify the high valuation hedge funds and banks had given it, it had to grow extremely fast. To do this, it started slashing rents and taking losses. WeWork tried justifying losses by claiming network effects would reap it profits later. But the effects were weak at best: tenants on New York’s Park Avenue would not improve the experience of tenants on nearby Fifth Avenue, and the effects of letting customers use sites around the world when they traveled on business would be “comparable to that of a global hotel chain with a loyalty program; it was not a tech-style network effect”.

Incredibly, “[i]n late 2015, Neumann demonstrated his regard for his financiers by letting off a fire extinguisher and spraying a prospective investor with white foam. Like a puppy who wags its tail eagerly even after being kicked, the investor proceeded to pour capital into WeWork the following year, driving its valuation to \$16 billion.”

Benchmark, which had invested in the company, could do nothing despite its apprehensions about WeWork’s corporate governance: “WeWork was not a public company, so its shares were hard to sell. WeWork’s founder had been granted super-voting rights, so shareholders lacked the clout to demand a change of direction.”

Uber

Later, Benchmark invested in Uber. Its founder Travis Kalanick gained more control of the board after Menlo Ventures invested with a board observer (rather than board director) seat. Then, Saudi Arabia’s national investment fund made a \$3.5bn investment in the company in a bid to diversify away from oil, which expanded the board and gave Kalanick the right to fill the new seats.

Kalanick then engaged himself in a ruinous war with an entrenched ride-hailing competitor in China, and a string of fiascos around Kalanick going to an escort bar and yelling at a taxi driver came to light.

The Benchmark investor Bill Gurley pointed out in a blogpost that late-stage investors had no downside due to buying liquidation preferences, so they encouraged their ventures to gamble for the upside. Most blog readers realized this referred to Kalanick’s unchecked price war in China. Gurley opposed the war, as it was different from the one with Lyft that he had financed: advertising wars were worth fighting only if winning was likely.

To rejig Uber’s governance, Gurley waged an astonishing corporate battle:

- First, he forced Kalanick to resign by threatening to make its internal investors’ memo public, which was critical of the CEO and would have turned board members against him.

- Second, he solicited a Son investment that concentrated power in the new CEO.

- Third, he filed a lawsuit claiming deceit, stating that Benchmark wouldn’t have approved Kalanick’s right to name 3 board directors if it had known of abuses like the trade secrets theft from Google.

In the end, Kalanick accepted Son’s investment and the governance change, conditional on Benchmark abandoning its legal offensive. Thus, he lost his influence on the board, and Benchmark dropped the lawsuit. The venture firm eventually made a cool \$6.9bn on its \$9mn investment.

The venture capitalist mindset

Subjective and data-driven investing

VC relies more on subjective judgment than most other areas of finance do: “Venture capitalists … seldom bother with spreadsheets. Academic survey work confirms that one in five venture capitalists do not even attempt to forecast cash flows when making an investment decision.”

Of course, many successful VCs do use spreadsheets. Most memorably, Yuri Milner relied on one to make a crazy-seeming bet on Facebook which paid off spectacularly.

Yuri Milner with Mark Zuckerberg in

2015, via

Fortune.

Yuri Milner with Mark Zuckerberg in

2015, via

Fortune.

At 100 million users, many investors felt that Facebook had reached a saturation point. However, Milner had a “voluminous spreadsheet on consumer-internet businesses in multiple countries, with cells tracking daily users, monthly users, the amount of time spent on the site, and so on” up his sleeve, which told him that social media websites usually made it to the top 3 websites of their country at their peak. Facebook wasn’t even in the top 5. Moreover, as Facebook was fat with venture capital, it hadn’t monetized itself as well as it could have; its Russian copycat VKontakte earned 5x more per user. Facebook hadn’t even considered virtual gifts, the chief revenue stream of social media websites in China.

Another example is Tiger Global, whose founders used their hedge fund training to focus on incremental margins to invest in firms undervalued by traditional VCs.

But Milner and Tiger are exceptions. A huge amount of VC decision-making is subjective. For example, Arthur Rock’s first reaction to Thomas Davis’ enthusiasm about the computer company Scientific Data Systems was “Jesus, I’ve gone into partnership with an idiot.” Davis and Rock had decided not to invest in computer companies, believing it was impossible to take on IBM.

If Mallaby is to be believed, what won Rock over was the founder Max Palvsky’s “warmth and informality”: “He could joke, flatter and cajole, and generally draw the best out of others.” Rock justified his reaction later: entrepreneurs with managerial magic can’t lose, because “[i]f their strategy doesn’t work, they can develop another one”. Rock reaped a bonanza when Xerox bought SDS.

Kleiner Perkins’ John Doerr told Brad Stone, who wrote The Everything Store, “I walked into the door and this guy with a boisterous laugh who was just exuding energy comes bounding down the steps. In that moment, I wanted to be in business with Jeff [Bezos].” Doerr received a handsome reward for his good judgment.

But subjective analysis can fail disastrously. Ctrl-F “I LOVE THIS FOUNDER” on Sequoia’s profile of FTX, which they took down after the crypto firm’s valuation crashed to zero following revelations of fraud.

Sam Bankman-Fried showing up to federal court in

2022, via Business

Insider.

Sam Bankman-Fried showing up to federal court in

2022, via Business

Insider.

To an extent, subjectivity in VC decision-making may be unavoidable. As Arthur Rock and Thomas Davis discovered when they set up their venture fund in 1960, most startups have no earnings or assets at the time they seek funding, so the traditional quantitative analysis methods of finance are useless. Rock had “made a habit of skipping over the financial projections in business plans and flipping to the back, where the founders’ résumés were presented”. The way he saw it, tech startups had only one asset: human talent, or what he liked to call “intellectual book value”.

But today, software startup founders require little more than free time and a laptop to ship a minimum viable product (MVP). VCs can use this MVP’s user data to guide their decisions (like Accel did, as I explain below).

The Accel “prepared mind” approach

Accel seems to have prioritized reducing subjectivity in investment decisions in a number of ways. From the beginning, its watchword was “the prepared mind”, from Louis Pasteur’s aphorism, “Chance favors the prepared mind.”

While Kleiner Perkins believed that the next great startup would by definition be unpredictable, Accel created management consulting-style reports on emerging technologies, then specialized in those it evaluated to be promising—its second round was entirely telecom companies, for example. This helped them avoid fads, therefore few of their ventures went bust like KP-backed pen-operated computer company GO, and Doerr’s other investments in next-gen laptops (Dynabook), human gene screening, anti-aging drugs, and designer chemicals did. They could also connect more deeply with founders due to their specialized knowledge; their partners followed a rule of knowing “90% of what founders are going to say before they open their mouths to say it”.

Accel’s deep reserves of specialized knowledge allowed them to foresee “adjacent possibilities”, ie, anticipate logical advances in technology. For example, their founder Jim Swartz “backed a videoconferencing startup in 1986, another in 1988, and a third in 1992; on two of these three bets, he made fourteen times his money”.

However, having surrounded themselves with intellectual leaders, they also tended to pass over uncredentialed founders. As a result, they missed the hugely profitable Cisco despite knowing of them and having a dedicated telecom fund. After Accel missed out on Skype, which had temperamental founders but was nevertheless growing fast, it course-corrected:

First, Accel must reach beyond the reassuring engineers whom it was used to backing. Experience showed that consumer internet companies were often founded by unorthodox characters: Yahoo and eBay had been founded by hobbyists. Second, the good news about consumer internet companies was that you could judge their prospects in a different way: you could look past the founders and analyze the data on their progress. The next time Accel came across an internet property that customers turned to multiple times per day, it should seal the deal no matter what.

Accel also recognized the “link between deliberately choosing a promising investment space, thereby reducing risk, and empowering the novices, thereby embracing risk”. As Jim Swartz said: “It is a lot easier to turn young investors loose if you know they are working fertile ground.” Since Accel had figured out in advance that Internet 1.0 had been about selling things over the Internet (Amazon, eBay), and Internet 2.0 would be about Internet as communications (Facebook), it knew that social networks were a low-risk field, and was more willing to make risky bets on novice founders.

Kevin Efrusy, a partner, said: “When I first arrived at Accel, I thought prepared mind was bullshit. It’s not.” It was Accel’s ruminative culture that helped it formulate these new guidelines. Later, it was these guidelines that helped them suppress their instinct against Sean Parker and Mark Zuckerberg, and invest in the fast-growing Facebook.

Innovation at Sequoia

Mallaby claims that more recently, Sequoia has taken a leaf out of Accel’s “prepared mind” book to improve the rationality of its decision-making. Their partner Roelof Botha realized that “Sometimes we felt that if a particular company had been there the previous Monday, or the subsequent Monday, our decision would have been different. That didn’t feel like a recipe for sustainable success.” So, he turned to decision science.

He made investors aware of their “loss aversion”: they were letting their companies exit prematurely, sacrificing upside. VCs sometimes showed “confirmation bias”, missing attractive Series B deals because they hated to admit they had been wrong in saying no to the same startup at the Series A stage. “Anchoring” (“basing a judgment on other people’s views rather than wrestling with the evidence and taking an independent position”, Mallaby explains) was another problem. At most VC firms, partners chat about the startups they’re evaluating before the formal vote to solicit advice and recruit allies. But this also encourages groupthink. Sequoia banned this canvassing.

Sequoia invested in the coder productivity sector (Unity, MongoDB and GitHub) with interesting reasoning around “the rise of the developer” that calls to mind Accel’s past focuses on telecom and social media companies: “Worldwide, a mere twenty-five million coders—one-third of 1 percent of the global population—were writing all the software that was transforming modern life. Anything that boosted the productivity of this small tribe would be immensely valuable.”

In Accel-like “prepared mind” spirit, Sequoia developed an “early bird” system: “seeing in the advent of the Apple App Store a trove of useful investment leads, Sequoia had written code that tracked downloads by consumers in sixty different countries”. This “digital sleuthing” alerted it to WhatsApp when it became the first or second most downloaded application in around thirty-five of the sixty markets. By conservatively assuming that the early bird system made Sequoia’s early investment in WhatsApp 10% more likely, Mallaby estimates that the piece of code was worth hundreds of millions of dollars.

Sequoia also experimented widely:

- First, realizing that angel investors’ understanding of the business landscape is dated, Sequoia adapted the angel investor model into a “scouts” program for current entrepreneurs whose wealth is tied up in company stock and is therefore illiquid (the reverse problem of veteran angel investors): “We give you \$100,000 to invest. We take half of the gains, but you as the scout get to keep the rest.” The biggest scout winners include Sam Altman’s Stripe and John Calanis’ Uber positions. Remarkably, one of the scouts was a carpet dealer whose job was to spot Iranian cofounders, recruited because of Sequoia’s “belief in immigrant grit: Moritz, Leone, and Botha were born in Wales, Italy, and South Africa, respectively, and three in five Sequoia-backed successes had at least one immigrant founder”. The carpet dealer brought to Sequoia’s attention Arash Ferdowsi-led Dropbox after he attended their pitch on YC’s demo day.

- Second, they opened a tech-focused hedge fund named Sequoia Capital Global Equities, or SCGE. Their reasoning was threefold: 1) it would allow them to gain from the mature (post-IPO) phase of companies it invested in; 2) tech-focused hedge funds were increasingly sidling up to Sequoia for advice, which meant Sequoia’s insights could be translated into public-market profits; 3) it would acquire the additional tool of “shorting” the losers of a digital disruption its inside knowledge predicted.

- Third, they started a wealth management fund named Heritage that has invested in assets ranging from stake in a chain of veterinary clinics to stock in Sequoia-backed companies like Stripe. This resembles McKinsey’s MIO Partners, though it’s worth mentioning that unlike MIO, which only invests for McKinsey’s current and former partners and other employees, Heritages takes on third-party clients. Another well-known wealth management fund (not affiliated with any investment or consultancy firm, etc) is ICONIQ Capital, which counts amongst its clients Mark Zuckerberg and some other Facebook cofounders and former chief executives.

- Fourth, they opened offices in China, India and Europe, usually entrusting locals to carry out day-to-day operations. Though their India shop met with initial setbacks, Shailendra Singh persisted and eventually landed the incredibly profitable Freecharge. (Freecharge’s founder, Kunal Shah, founded and currently heads the popular CRED.)

Fun trivia

- Georges Doriot, the founder of American Research and Development, also founded INSEAD.

- Reid Dennis, one of SV’s earliest investors, wagered his entire life’s savings on a tape recorder company, telling his wife that “if she was good enough to get me, she ought to be able to get somebody else to support her if anything happened”. (The company became wildly successful, earning him \$1mn in 1958.)

- “Venture capital” is an abbreviation of “adventure capital”, a reflection of the fact that it is riskier than most other financial investments.

- Robert Noyce, who later led the Traitorous Eight in founding Fairchild, agonized over his decision to “betray” Shockley. The son of two Congregational ministers, Noyce asked himself: “What would God think?” Finally, though, he decided to accept Arthur Rock’s \$1 million funding package to found the company.

- Rock invited his alma mater Grinnell College to participate when Intel’s investors were being selected, and part of the reason for the college’s unusually large endowment today seems to be its early investments in Berkshire Hathaway and Intel. See this article for more.

- Arthur Rock formulated Rock’s law (also called Moore’s second law): “the cost of a semiconductor chip fabrication plant [a “fab”] doubles every four years”. To the best of my knowledge, this is surprisingly accurate. Today, the cost of a cutting-edge fab is \$20 billion.

- Clayton Christensen coined the term “innovator’s dilemma” to describe incumbents having too much of a stake in the status quo to push disruptive products. The best example is Xerox, Intel, National Semiconductor and HP deciding not to build the PC, despite recognizing its profitability. “Xerox worried that a computerized paperless office would harm its core photocopying business. Intel and National Semiconductor feared that making a computer would put them in conflict with existing computer makers, which were among their top customers. HP fretted that building a cheap home computer would undercut its premium machines, which sold for around \$150,000.” Apple, therefore, was able to use Xerox PARC’s research to start the personal computing revolution.

- How important were networks to VCs? In an interview with Mallaby, Don Valentine called the bar Wagon Wheel, where engineers chatted with VCs about up-and-coming technical products and protocols, his “graduate school”.

- A partnership that KP had brokered between one of its ventures and a chipmaker broke up because the chip was too expensive for too little benefit. Then, the chipmaker started collaborating with the venture’s competitor, endangering the intellectual property KP’s venture had already shared with the chipmaker. KP agreed to pay its venture \$500,000—no equity asked—presumably because preserving its reputation was just worth that much. For scale, this was nearly half what the wildly successful Ethernet company 3Com had raised in its Series A round.

- Max Levchin was prepared for Confinity and X.com to merge at a 40:60 share. Then, Musk taunted him, “Just so you know, you’re getting a great deal. This merger of unequals is a steal for you guys.” Levchin huffed off, and had to be placated with a 50:50 deal. Musk’s taunt cost him millions.

- Vinod Khosla, earlier co-founder of Sun Microsystems and general partner at KP, now founder/partner at Khosla Ventures, is described as an ambitious contrarian: “As a boy in his native India, he rebelled against his parents’ religion, declined to follow his father into the army, and refused an arranged marriage. On his wedding day, he set his watch alarm, declaring that the religious portion of the ceremony had to be done inside thirty minutes.” When Khosla learned that Stanford Business School required 2 years’ work experience as a requirement for admission, “he did two jobs at once and declared after one year that he had met the requirement.”

- Paul Graham got to know the Collisons “because, as a high-schooler in Ireland, Patrick had emailed him with coding questions—‘I had no idea he was a high-school kid, because his questions were so sophisticated,’ Graham recalled later. When Patrick had come to the United States to interview at colleges, he had stayed at Graham’s house; and Graham had gone on to introduce him to a pair of YC founders, sparking the formation of the Collisons’ first startup.”

- Menlo Ventures’ Shervin Pishevar was the Uber-cheerleader (see what I did there?): he became a board observer after investing in the ride hailing app, and shaved the company logo into his hair.

{kind=link}