Sex as portfolio diversification for genes

Selfish genes

In general, animal behavior which seems altruistic on first blush is actually selfish. For example, when a gazelle jumps up and down upon seeing a predator, it looks like it is sounding an alarm for its herd while making itself more conspicuous, but really it’s sending the predator a credible signal that it would be hard to catch. Living beings don’t reproduce for the good of their species. Rather, selfish genes shape the behavior of what Richard Dawkins calls “survival machines” — the living beings carrying those genes — to maximize the likelihood of said genes getting passed on.

(Actually, while we’re at it, what is a gene, really? There are forces scrambling the genetic material (DNA) that gets passed on to each generation. A gene is a chunk of the DNA that is small enough not to get scrambled for several generations. Genes often influence our makeup — our eye color and blood group, for example — but they also may not. Large sections of our DNA don’t seem to be doing anything.)

It’s important not to anthropomorphize the genes here. They don’t want or plan anything. Rather, the genes that increase the likelihood of getting passed on get passed on. For example, if a gene mutates to camouflage a butterfly against flowers, that butterfly is less likely to get eaten before reproducing — and ditto for its descendants. Soon, its descendants outnumber those without the camouflage mutation. The gene for the mutation has spread among the species. It has “selfishly” grown in the gene pool at the expense of other genes coding for wing color.

The logic here is closely related to my favorite explanation for why the Internet has become more clickbaity over time. It’s not that the behavior of content creators has changed, but that the creators who (knowingly or not) optimized their content for getting more clicks got more clicks. Rewarded with revenue, they hired ever greater hordes of copywriters to write for them. In his microeconomics textbook (available for free), David Friedman uses similar reasoning to explain why the classical assumption that participants in the market are rational is not so unreasonable after all:

[W]hy the assumption works better than one might expect is that we are often dealing not with a random set of people but with people who have been selected for the particular role they are playing. Consider the heads of companies. If you selected people at random for the job, the assumption that they want to maximize the company’s profits and know how to do so would not be a very plausible one. But people who do not want to maximize profits, or do not know how to, are unlikely to be chosen for the job; if they are, they are unlikely to keep it; if they do, their companies are likely to become increasingly unimportant in the economy, until eventually the companies go out of business. So the simple assumption of profit maximization plus rationality turns out to be a good way to predict how firms will behave.

A similar argument applies to the stock market. We may reasonably expect that the average investment is made by someone with an accurate idea of what companies are worth–even though the average American, and even the average investor, may be poorly informed about such things. Investors who consistently bet wrong on the stock market soon have very little to bet with. Investors who consistently bet right have an increasing amount of their own money to risk–and often other people’s money as well. Hence the well-informed investors have an influence on the market out of proportion to their numbers as a fraction of the population.

The mystery of sex

Selfish genes make it obvious why reproduction happens — that’s how the genes get passed on, dummy! But it’s mysterious why sexual reproduction happens.

From the gene’s point of view, asexual reproduction is straightforward. You spend some resources and create another “survival machine” to carry your genes. But sex is complicated. You must happen upon a mate. And, of course, you never just happen upon a mate. To attract one, you have to grow silly plumes that make you more conspicuous to predators. To fight for one one, you have to grow massive claws that take up half of all your available energy. Growing babies is a drag, but sexual reproduction ain’t a free lunch for males, either. As Douglas Emlen writes in Animal Weapons, antlers in moose are “every bit as costly to a male as reproduction was to a female: the cost of building and using antlers was energetically and nutritionally equivalent to the cost of producing and nursing two fawns to weaning.” At best, sexual reproduction is just as expensive as asexual reproduction. At worst, it requires a double coincidence of wants with all its transaction costs. So, why is it so common?

I found Richard Dawkins’ answer in The Selfish Gene somewhat incomplete. He argues that “if sexual, as opposed to non-sexual, reproduction benefits a gene for sexual reproduction, that is a sufficient explanation for the existence of sexual reproduction. Whether or not it benefits all the rest of an individual’s genes is comparatively irrelevant.” I am prepared to accept his second sentence — it is not the collection of genes in an individual that is the unit of selection, but individual genes themselves. But it wasn’t clear to me why sexual reproduction would benefit a gene for sexual reproduction. If anything, the gene should hope that another gene suppresses its awkward sexual urges, and inexpensive asexual reproduction can go on as usual.

This post is my stab at an explanation for sexual reproduction. I wrote it because it’s different from those I found from a very quick literature review, but I wouldn’t be surprised if it already exists in a more fleshed-out version somewhere.

But first, a primer on diversification.

A crash course on diversification

Say that you’re an investor and like a copper mining company and a candy chain. You like them equally — you expect them to deliver the same return on investment. The logic of diversification says that even though you’re indifferent between the two companies, you should split your investment between them rather than put all your eggs in one basket. This is because the events that could hurt the copper company (like a weakening housing market in China) are unlikely to affect the candy chain, and vice versa. In other words, the prospects of the copper company and the candy chain are mostly uncorrelated. (Of course, in an ideal portfolio, your investments would be negatively correlated. If you’re investing in a copper company, you would like to also invest in a promising oil company. This would hedge against the risk of carbon tax cuts, which make electric vehicles unappealing and tank the price of their components, but raise the demand for oil.) Okay, but what if your two favorite investments are positively correlated? That is, if one does well, the other does too, and if one does poorly, the other does too. Turns out you should still split your investments between them. For example, alongside copper, investing in a good zinc company is not a bad idea. This is because the zinc and the copper company are at least a little different. Both of them can go belly up together for a common reason, but there is at least a sizable chance that one is unaffected when the other flounders.

Note that if you invest in equally promising companies, i.e., companies with the same expected return on investment, you don’t make more with diversification than you do without. You only reduce the variability in possible outcomes. There is a lot of uncertainty about what a copper company is going to be worth six months from now. But there is relatively less uncertainty about what the weighted average of five hundred different companies’ stocks is going to be six months from now.

A gene will diversify its neighborhood

An interesting idea from The Selfish Gene is that of the genetic climate of a gene, i.e., the rest of the genes in the body it occupies. They are as much a part of the gene’s environment as the sun, water and temperature. A gene’s genetic climate can affect its success as much as (or more than) the actual climate. Being in the same body with a gene that causes cancer in infancy would be disastrous.

My theory is that sexual reproduction is a kind of diversification for the genes causing sexual reproduction. In asexual reproduction, the genetic makeup of the offspring is nearly identical to the parent’s, modulo errors in copying DNA. A gene has to pin all its hopes on its neighbors not messing up. But this is dangerous: you’d rather be in several genetic climates than one, all else equal. This way, even if you have incompetent neighbors in one genetic climate, your odds of survival aren’t dashed.

But there’s a caveat: you will diversify your genetic neighborhood if all else is equal. You don’t want to move into a much worse neighborhood (just like you wouldn’t buy a crappy stock in the name of diversification). This turns out not to be a problem, however. In the offspring’s body, half your neighbors will be your old ones. The other half will be from a genetic climate that was selected for fitness in the same external environment as your old genetic climate. The offspring’s other parent is not going to be more or less fit, on average. So, you have no a priori reason to think that your new neighbors are any better or worse than your old ones — similar to how, if you have no other information, you cannot distinguish between two students who got the same GPA, went to the same school, and come from the same socioeconomic background.

There is one last kink to iron out. Remember that diversification does not increase the expected return on your investment. It only tightens the variability of possible outcomes. In other words, you diversify only because your appetite for risk is not bottomless. Why should we assume that genes are similarly risk-averse? Why don’t genes pursue the high-risk, high-reward strategy of sticking with their genetic neighbors forever?

The first response to this is that there are asexually reproducing creatures. Maybe they’ve found a niche of the Earth that seldom changes for the worse, so never changing your neighbors isn’t that risky.

“Sure”, I hear you say. “But what explains the tremendous success of sexually reproducing creatures compared to asexual reproducers? Sexually reproducing creatures are everywhere. The asexually reproducing, not so much. Why?”

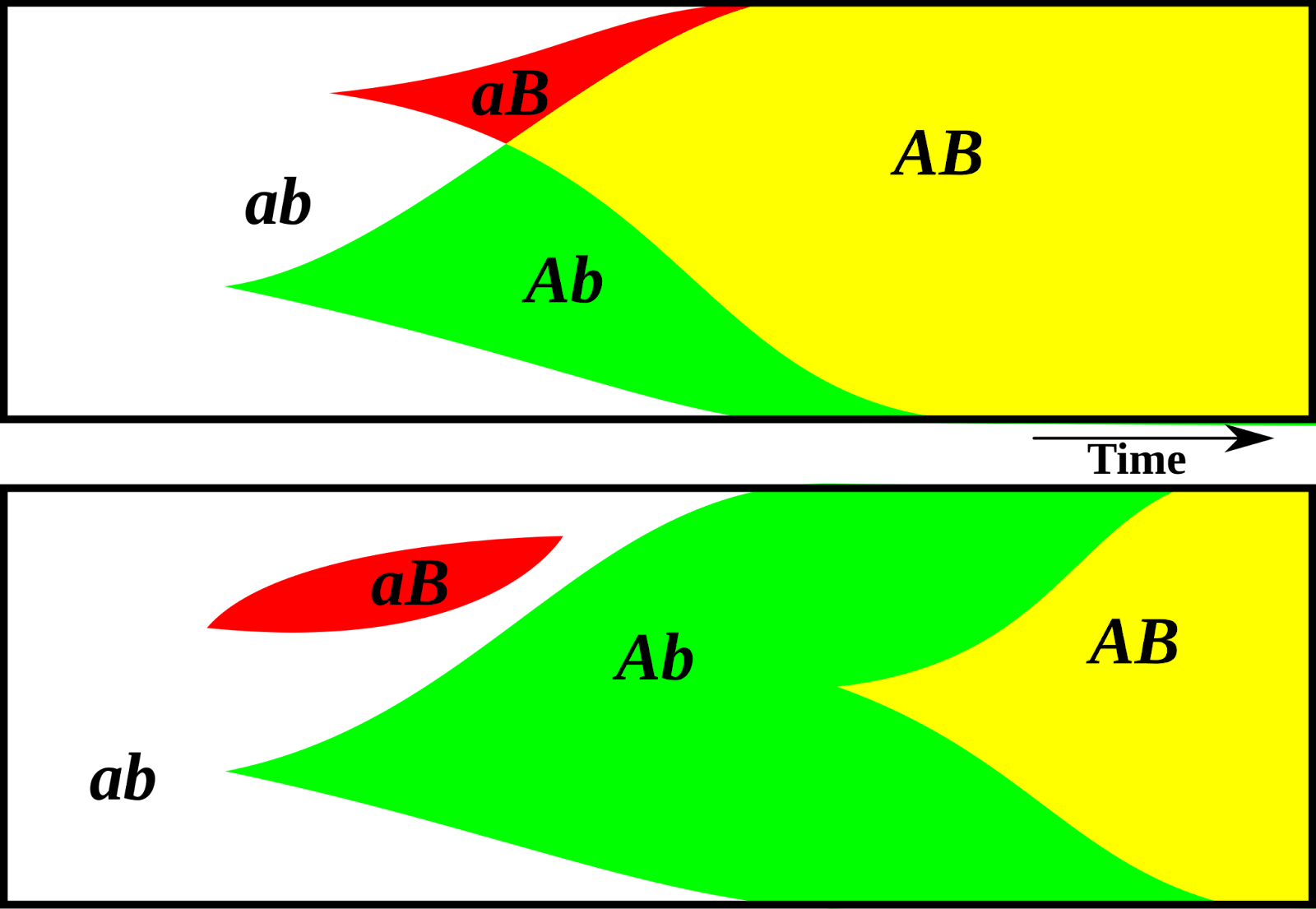

The spread of helpful genes A and B in sexually reproducing (top) and asexually reproducing (bottom) species. Via MykReeve on Wikimedia.

{kind=link}

Clonal interference is one answer. If there is an adverse change in the external environment, an asexually reproducing creature can save itself by mutation. However, the rate of mutations in every generation is typically very low — DNA copying is a stunningly high-fidelity process. Now imagine that to avoid dying out due to the environment change, multiple different mutations are required. Then, all of them must arise independently on the same lineage of creatures — this starts to look outstandingly unlikely as the necessary number of mutations increases. What’s worse is that if two lineages independently develop helpful mutations, they may even start competing with each other. But in sexually reproducing creatures, helpful mutations can arise in different members of the population, and spread all over the population as these lucky creatures’ descendants mate with each other. Sexually reproducing species avoid getting wiped out by responding to changes more quickly. So, we see more of them in nature.

But we needn’t turn to a different flavor of argumentation altogether — if we follow the portfolio theory thread, bet hedging explains why genes would be risk-averse. In investing, what matters isn’t arithmetic mean returns, but geometric mean returns over time. The key insight (this is also the intuition behind the Kelly criterion) is that multiplication of probabilities punishes variance severely.

A simple example: consider two strategies, a “risky” one which produces either $2x$ or $0x$ offspring each generation with equal probability, and a “conservative” one that reliably produces $0.9x$ offspring each generation. Over one generation, the risky strategy looks better: expected value of $1x$ over $0.9x$. But over multiple generations, the risky strategy might go: $2x \times 2x \times \cdots \times 0x = 0$. Meanwhile, even after ten generations, the conservative strategy is producing over $0.33x$ offspring.

The risky strategy goes poof if it hits one bad generation, but the conservative strategy persists. And in environments that aren’t stable, it tends to win out. So, why is sexual reproduction so common? I guess most environments are unstable.